32 MIN. READ

In the business field, the pillars of security, transparency, reliability, and efficiency stand as the basis of success. Security ensures the protection of sensitive data, ensuring trust with clients and safeguarding against cyber threats. Transparency builds credibility, bringing confidence to stakeholders and customers alike. Reliability is the anchor of customer loyalty, creating consistent performance and dependability. Meanwhile, efficiency drives productivity, enabling businesses to adapt swiftly to market demands. Together, these elements form an inseparable link, defining the resilience and competitiveness of a business, all of which is highly achievable through blockchain transactions.

Traditional transactions in business rely on centralized systems, often prone to delays, intermediaries, and vulnerability to fraud. In contrast, transactions on the blockchain revolutionize this landscape by offering decentralized, secure, and transparent processes. Old-fashioned transactions are slowly being overtaken by the revolutionary system of payments through blockchains, and there are many use cases and benefits to show why exactly that is. Any business with the mindset to succeed in the current competitive world should have this revolutionary business strategy in mind, and this guide is here to show you all the basics, benefits and use cases of blockchain payments and how they can reshape your business.

The blockchain technology is a revolutionary decentralized system that ensures secure and transparent transactions across a network of computers. It acts as a digital ledger, recording transactions. Unlike traditional ledgers, relying on pieces of paper or computer documents, the blockchain record system is impossible to be tampered with or even deleted forever.

Transactions through the blockchain system work perfectly because of how they are processed. Once the transaction is requested, it is turned into a block, as part of the blockchain ledger. All network-connected computers, also known as nodes, need to verify this transaction through various validation processes, which this article will discuss in more detail further below. Once that process is done, the transaction block is linked to all previous blocks, thus cementing its place within the blockchain records and is available transparently for public access. This marks the completion of the crypto minting process on a blockchain and basically describes how the blockchain technology works.

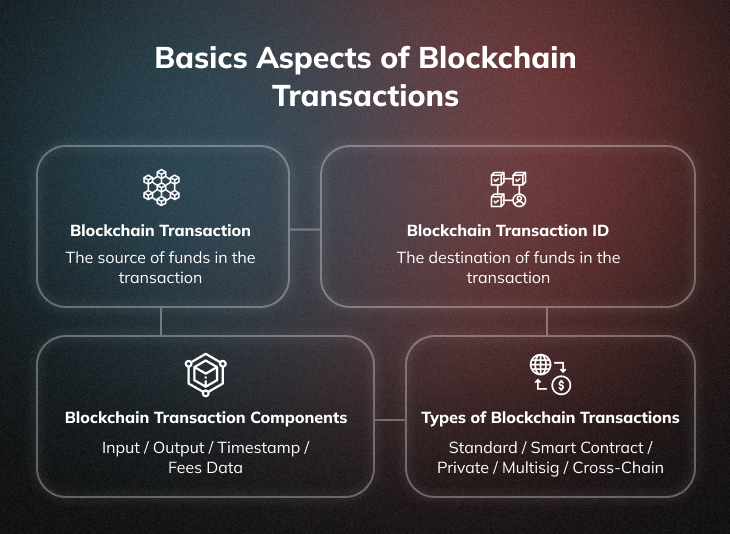

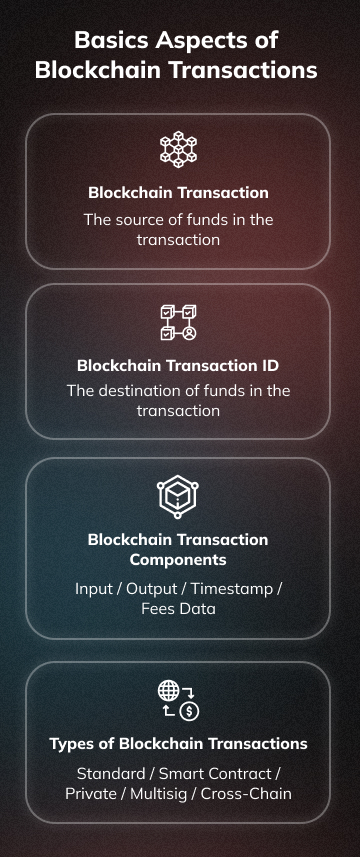

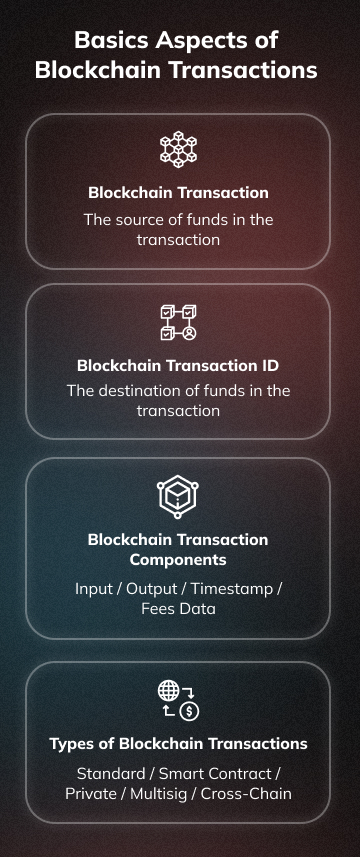

The blockchain technology has a lot of small details that need to be studied before you can see the bigger picture. But knowing those basics means that your business has a leader with the essential knowledge on blockchain and transactions to push it forward. For example, a blockchain transaction is any attempt to transfer digital assets from one wallet to another, and these come with personal transaction IDs. These IDs, also called hashes, act as a unique identifier, or almost like a receipt. They represent long alphanumeric strings and serve as a digital fingerprint for transactions.

Now, a blockchain transaction contains a lot of information within it. Some of the key components are:

Additionally, there are different types of transactions in the blockchain. Standard transactions represent uncomplex transactions of cryptocurrencies between two wallets. Transactions involving smart contracts can involve and execute programmable actions which are predefined in the contracts, eliminating the need for middlemen. Private transactions are very specific and hosted on specific blockchains which remove the transparency of details like sender and recipient details. Multi-signature transactions, or multisig transactions, quite forward, require multiple digital signatures to authorize the transaction. There are also cross-chain transactions which enable transactions between different blockchain networks and ecosystems.

Furthermore, each transaction on the blockchain is associated with a unique identifier known as a blockchain transaction ID, which is crucial for tracking and verifying the specific details and status of individual transactions within the vast network of blockchain operations. Knowing these important aspects about them, let’s see how exactly they work.

As blockchain becomes integral to various industries, a business owner’s understanding of it is not just beneficial but essential for sustained success of the business. To implement blockchain network within your business is a very smart decision in the long run, but to be confident in doing it, you should be understanding of the lifecycle of transactions, the roles of nodes and miners and what transaction pools are. This will ensure you make informed decisions, reduce or even remove any chances of fraud risks and in general to benefit from the transformative potential that blockchains have to offer.

The role of nodes and miners is vital for the blockchain operations. Although similar, both components represent different things with distinctive roles. A node is a computer containing a copy of the whole blockchain with all its transaction records. These nodes validate transactions with other nodes within their network. Miners, on the other hand, are a subset of nodes and are the equipment that uses computational power to solve complex mathematical equations/puzzles in order to validate transactions and to create new blocks.

Digital wallets are a unique application to store, manage and interact with cryptocurrency and NFT assets. It is an essential security place for all Web3 assets, with incredible security in place to protect the user’s savings. Users can store, send and receive cryptocurrencies, create backups and recoveries of their wallets and can have an elevated sense of security around their owned assets (through private keys and various encryption methods).

There are two types of wallets. Any digital wallets connected to the internet and accessed through a web browser or a mobile app are called hot wallets. These come as a web version, desktop apps or mobile apps. And there are cold wallets, mostly in the form of USB ledgers, and are considered more secure because the private keys and the assets are stored offline.

A transaction pool, or mempool, is a temporary storage place where blockchain unconfirmed transactions are stored before being confirmed and included in a block. It basically acts as a queue for pending transactions on the blockchain. Miners select transactions from the pool, verify them, and add them to the next block. Usually, transactions with higher gas fees or better incentives get prioritized for inclusion in the blockchain.

You are looking into expanding your business into the Web3 realm, and you recognize the power of blockchains and how they can transform the way your business operates and executes transactions. That’s a great first step and following is the understanding that not all blockchain transactions undergo instantaneous confirmation. There are two types of transactions in this sense and those are the unconfirmed and the confirmed ones.

Comparing unconfirmed and confirmed blockchain transactions makes it obvious that if the transaction is important for you, then it is always better to include a higher gas fee to ensure that it will be processed and that it will happen faster. Otherwise, you’re risking having an unconfirmed blockchain transaction with long wait times and even potential dropping, which will complicate your business transactions.

Understanding the difference between those types of transactions is therefore important for your business. It will allow you to plan ahead and optimize your operations’ efficiency by keeping in mind that your transactions might not go through, and you can have a plan B to ensure smooth business operations.

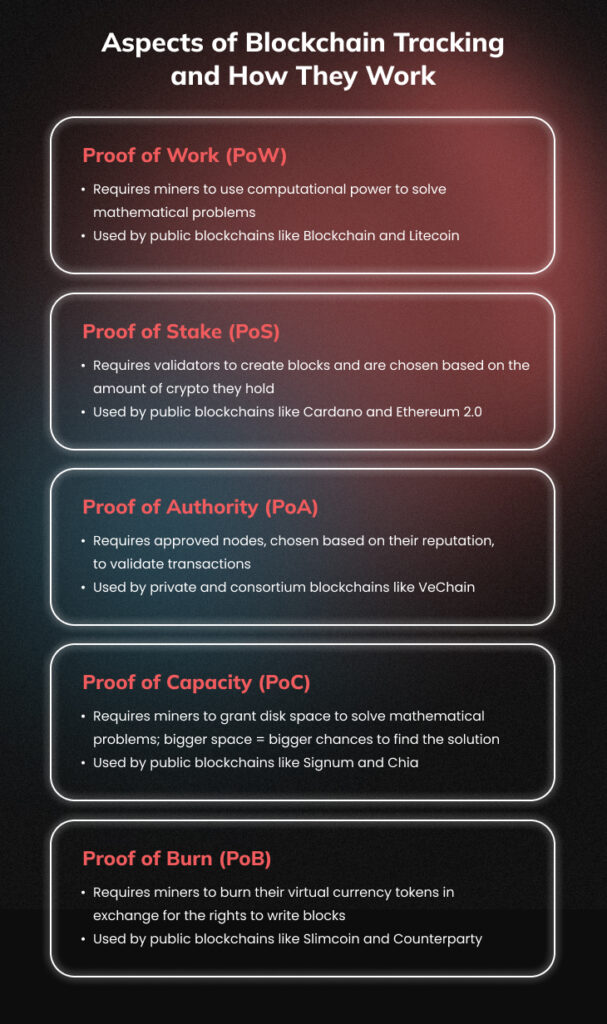

Consensus mechanisms are vital protocols that ensure smooth transaction operations within blockchains. These consensus mechanisms enable security, trust and efficiency for blockchains. They work towards immutability for all digital ledger records and also contribute towards fair token distribution, be it through transactions or rewards to miners for their work on the verification process. There are many consensus mechanisms, each used by different blockchains for their own benefits, and it’s important to choose wisely when associating your business with one of them for important reasons.

Each consensus mechanism is used for a different type of blockchains, and although this topic extends beyond this article’s intended focus, it is discussed in more detail in our Ultimate Guide on Blockchains (2023). For now, let’s explore the most used consensus mechanisms that most blockchains rely on.

The PoW consensus mechanism is probably the most famous out of all, because it is directly associated with the Bitcoin blockchain. PoW enables decentralization by eliminating the need for central authority and requires miners to do the work. They are required to solve complex mathematical puzzles to create a new block to the blockchain, for which the miners are then rewarded with the associated fees or newly acquired crypto. However, this consensus mechanism requires very high computational power, which is often associated with burning a lot of electricity resulting in expensive prices.

Proof of Stake is the second most famous consensus mechanism used in blockchains. It doesn’t require miners to solve complex mathematical puzzles. Instead, it relies on validators, which stake their cryptocurrency coins and are then chosen to create new blocks on the blockchain. In PoS, the higher the staked coins = higher chances of being selected to do the work. As a reward, validators receive transaction fees or new cryptocurrency. This mechanism is strongly associated with more energy-efficient methods of work and is sometimes favored over PoW.

There are over ten well-known consensus mechanisms recorded nowadays that many blockchains operate with. The Proof of Authority (PoA) mechanism is used by mostly private blockchains and operates by choosing the nodes with highest reputation within their network to validate transactions. The Proof of Burn (PoB) is another interesting consensus mechanism which involves miners burning/destroying part of their cryptocurrency for some rights to create blocks on the specific blockchain. This is an experimental method but is recognized as the new PoW that doesn’t create any energy waste.

It’s worth noting that as blockchains evolve, many of those mechanisms might be combined, developed or replaced completely. There are some blockchains which combine two or more consensus mechanisms to try different ways of operating. And nowadays, many people are concerned about the carbon footprint that blockchains are leaving behind. This urges blockchains to go through trial and error with new technologies, in order to stay used and loved by their users.

Understanding transaction fees, how they are determined and why they exist is very important for your business. With that knowledge, you will be able to optimize the cost-effectiveness of your transactions and ensure their timely processing. It’s important to monitor the blockchain you are using and the fee structure of it, so that you can properly adjust them in your transactions. It’s also important to adjust the fees based on the transaction urgency. Fee management is essential for the overall transaction performance and the reliability that your business wants to project onto your clients.

| Optimize cost-effective transactions for your business | Ensure that transactions are added to the blockchain in time |

| Avoid overpaying fees for your transactions | Become an expert in fee management |

| Having prohibitive transactions for your business | Receiving slow verification times or dropped transactions |

| Paying excessive fees for your transactions | Losing control over management of fees |

The most important aspects around transaction fees are how they are determined, their fee structures in the different blockchains available and what the role of gas in the ETH blockchain is.

The determination of transactional fees is dependent on several factors:

Finally, the blockchain protocol on how fees are determined is yet another important factor. However, each blockchain has its own rules on what the fee structure is, and the next point will discuss this in more detail.

Blockchains differ from each other in various ways, and one of those is how they structure their fees. When selecting the best blockchain for your business, it is important that you also consider the variety of fee structures that you can sign up for. For example:

There are numerous other blockchains, each implementing its own fee structures, some more complex than others. One of the most important blockchains is that of the Ethereum, and it’s interesting to look at what the role of gas in that blockchain is.

The Ethereum blockchain is the second largest blockchain, and if you want to implement blockchain transactions into your business, it’s important to also know about the role of gas in ETH before choosing that blockchain. ETH gas is what must be paid for transactions to be processed, or for users to use smart contracts on the ETH blockchain. ETH gas is called gwei, short for gigawei, which is a billionth of an ETH. All gas on ETH is paid in the Ethereum cryptocurrency.

Ethereum’s gas fee structure depends on three factors. Firstly, the transaction complexity represents the gas needed for transaction processing. Then, the base fee is introduced as the minimum price required for a transaction to be considered for processing. And finally, the priority fee, which is an incentive fee aimed to expedite the processing time. By considering these factors, you can prevent your fees from snowballing into larger and unnecessary expenses.

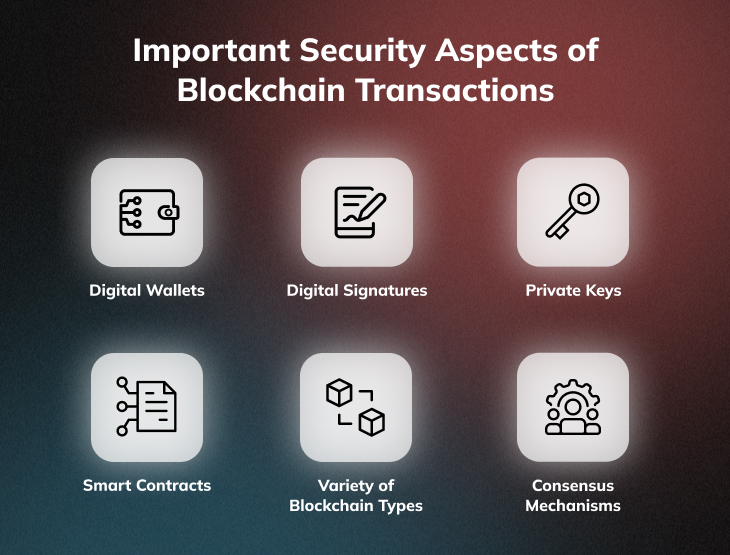

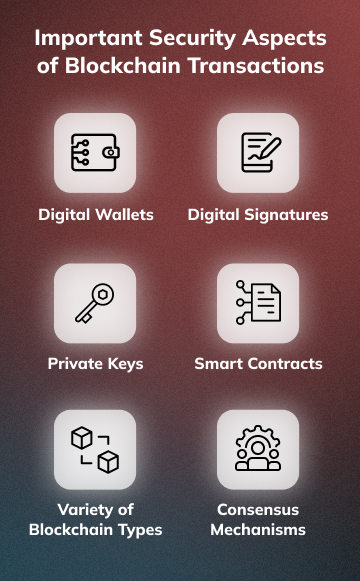

Blockchain’s powerful security protocols ensure trust and integrity in transactions, establishing a professional environment for businesses. The tamper-proof nature of blockchain safeguards against fraud and tampering, instilling confidence in financial interactions. This is especially beneficial for businesses as they handle a great amount of user data, personal business plans and sometimes large transactions.

Some of the most important security aspects of blockchains are mostly things the naked eye doesn’t understand at first sight, or it doesn’t even see, as there are a lot of security protocols running in the background that users don’t get to interact with. Those are all the operations behind the beloved digital wallets, digital signatures and private keys that all play a role in protecting your crypto funds. They are also the smart contracts and the consensus mechanisms in the different types of blockchains that ultimately process transactions in a fast and efficient manner to work in your best interest. Of course, there are many other important aspects, so let’s look at some of them up next.

Each blockchain has its own way of formatting addresses:

In blockchains, key management involves securing private keys for cryptographic control over digital assets. Businesses can implement robust practices like hardware wallets, encrypted storage, and regular audits to ensure the integrity of their keys. This proactive approach safeguards against unauthorized access, enhancing security for blockchain-based assets and transactions.

There are many security threats that can target blockchains, but there are even more ways to enhance a blockchain’s resilience against them, to the point where it’s basically impossible to tamper with them and their records.

Security Threats:

Mitigation Strategies:

Smart contracts and automated transactions on the blockchain are revolutionizing business operations in the Web3 era. These self-executing contracts, powered by blockchain technology, automate and enforce agreements, cutting through traditional intermediaries. By including prewritten rules in their code, smart contracts ensure transparency, security, and efficiency in transactions. Businesses, through these automated transactions, benefit from reduced costs, minimized errors, and accelerated processes. From supply chain management to finance, medicine and even legal processes, embracing smart contracts in your business can unleash a new era of innovation, empowering your businesses to thrive in its field.

Looking up transactions on the blockchain reveals a wealth of data, including the sender, receiver, amount and type of cryptocurrency, transaction ID (hash), and timestamps. The question of how to track blockchain transactions is an excellent opportunity for businesses to stay updated on their own transactions, validate the credibility of business partners, and ensure the integrity of the business itself.

Tracking blockchain transactions is easy thanks to blockchain explorers. This type of software allows users to transparently obtain data about transactions, blocks, addresses and other blockchain-based data.

A blockchain explorer is the web-based tool or interface that businesses should always have in mind when operating with blockchain-based transactions. This software allows businesses to explore and interact with all sorts of blockchain data. It provides a transparent way to view details about transactions, blocks, addresses, and other relevant information on a specific blockchain. Blockchain explorers are commonly used to track transactions, verify payments, and explore the blockchain transaction history in a user-friendly manner, creating easy access to important decision-making.

Interoperability in blockchain refers to the seamless exchange of information and value across different blockchain networks. It enables these blockchains to communicate and share data across each other, enabling collaboration among decentralized ecosystems. Cross-chain transactions, a vital component of interoperability, can thus enable assets and information to move between different blockchains. This system improves efficiency, scalability, and user experience.

Projects like Polkadot and Cosmos are a great example of blockchains that aim to facilitate interoperability by creating frameworks that enable secure and efficient communication. Including interoperability can be innovative for the wider adoption and evolution of decentralized blockchains as it will ensure a broader connected and collaborative blockchain network around the world, providing businesses with more opportunities to grow.

In the rapidly growing world of blockchains, regulatory compliance, notably KYC (Know Your Customer) and AML (Anti-Money Laundering), is essential. KYC is a process businesses use to verify the identity of clients for security and compliance. AML, on the other hand, is a regulatory framework preventing illicit financial activities by ensuring transparency and accountability in transactions, such that decentralized blockchains offer.

Governments globally are increasingly emphasizing these standards to ensure transparency and lower chances of risks for businesses. Ensuring that these regulations are strictly followed will not only solidify the trust between your business and your clients but will also position you for sustained success in the rapidly evolving blockchain ecosystem.

Businesses can overcome competitors by leveraging blockchain technology, offering enhanced transparency, security, and efficiency. Embracing blockchain not only future-proofs operations but also positions businesses as innovative, trustworthy, and forward-thinking, distinguishing them in their industries.

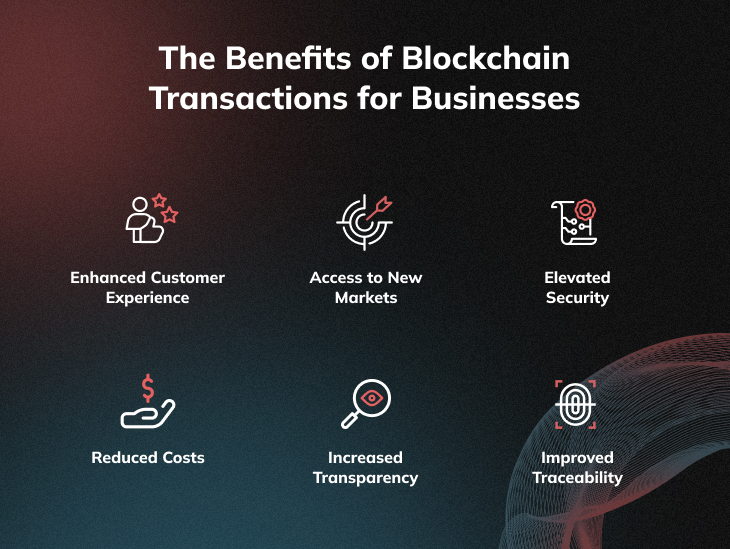

The transformative potential of blockchain empowers businesses to optimize workflows and provide original services to an even wider circle of customers. Blockchains enable businesses in various industries to be more successful than ever. Below, you can find some of the benefits that these types of transactions bring to businesses.

Customer experience is elevated by blockchains as they ensure transparency, security, and efficiency. Immutable records and smart contracts enhance trust and reduce disputes. Faster, low-cost transactions and decentralized systems empower customers, while personalized, blockchain-enabled services create a seamless and innovative experience. A business embracing blockchains can transform the way its customers interact with it, resulting in a stronger sense of loyalty, by implementing various Web3 projects like NFT loyalty programs.

Blockchains open doors to new markets for businesses by eliminating geographical barriers and enhancing cross-border transactions. Businesses can go into global partnerships with confidence due to smart contracts. This borderless accessibility expands the list of opportunities for businesses willing to implement blockchains, by bringing businesses diverse audiences and expansion to their market presences.

Enhanced security is provided for businesses by blockchains through cryptographic techniques and decentralization. Immutable records prevent tampering, and consensus mechanisms ensure data integrity. Private keys and smart contracts bolster authentication and reduce fraud risks. This reliable security framework builds trust, safeguarding sensitive information and transactions for businesses willing to go the extra mile.

Blockchains reduce costs for businesses by eliminating any unnecessary middlemen, streamlining processes, and minimizing the need for manual verification. Because smart contracts automate agreements, administrative expenses are significantly cut and because there is no need for a centralized infrastructure, transaction fees are overall lowered. This cost-efficient approach positions businesses for sustainable growth and increased profitability.

Transparency is provided for businesses by blockchains through an immutable and publicly accessible ledger of transactions. This creates a trustworthy reputation for your business as real-time visibility into processes and supply chains is enabled for partners and customers. Decentralized consensus ensures data accuracy, reducing the potential for fraud.

Blockchains improve traceability for businesses by creating an unalterable record of transactions and events. This transparency allows seamless tracking of products in supply chains, or keeping track of important records, like in the healthcare industry. Enhanced traceability not only meets regulatory requirements but also boosts consumer confidence, reinforcing businesses’ commitment to quality and accountability.

Having understood the basics of how transactions function in real-life scenarios, you might be wondering how to properly implement this knowledge in your business. Maybe you’re wondering whether this can be done for your specific industry at all. The good news is that because of many businesses taking that leap of faith, we have a great list of use cases to learn from. And what any blockchain-oriented person might know is that any of the leading industries can benefit from a blockchain system, one way or another. Take this list of specific industry use-cases for example.

A business in the supply chain management industry can implement a blockchain system in many ways. A blockchain for this industry is highly profitable for tracking products from production to delivery. This system can enable a business to look up product data in seconds, compared to having to track it in a standard way, which might take days to track down a product.

Blockchains are also very suitable for a business in the financial services industry. These businesses can profit from the automation of smart contracts and in general the whole concept of the blockchain being a digital ledger. A financial services business is most likely to handle a big amount of confidential data, which is more securely stored in a blockchain than traditional storage.

Voting systems, especially for governments, can benefit from a blockchain system implementation greatly. The decentralized nature of a blockchain will allow for all votes to be easily verified and can therefore prevent fraudulent activities. Having this system set in place might encourage more people to vote as they will have an enhanced sense of trust in their government.

Intellectual Property (IP) is any invention (literacy, art, design, symbol, name, image) used in commerce. IP is protected by laws through patents, copyrights, trademarks which grant the creator with exclusive rights to reproduce, distribute and use their creation in any way they wish. Those can also be NFTs.

Royalties are directly associated with IPs, as they act as compensation for the use of those IPs by secondary parties. When a licensee benefits from that IP directly, they have to compensate the IP’s owner. The terms and conditions of the usage and the amount of the royalties are defined by the IP owner. Royalties can also be received through any secondary sales of your NFT collection.

The blockchain technology can revolutionize the identity verification industry. Businesses can leverage blockchains to store and manage identity information, ensuring privacy and reducing the risk of data breaches. Immutable records on the blockchain improve the accuracy and integrity of identity data. Additionally, users gain greater control over their personal information, as access is granted only through cryptographic keys.

Blockchain technology in the food safety industry ensures transparency and traceability throughout the supply chain. By recording every step from production to consummation on a fixed ledger, businesses can easily identify and address issues like contamination or recalls. This enhances accountability, reduces fraud, and ensures that consumers worldwide receive the best products available on the market.

A blockchain system can bring a business in the retail and e-commerce industry forward through each benefit that it has. This type of business can receive a traceable and secure supply chain management system. It can also bring diverse payment methods to their customers, and speaking of customers, businesses in the retail and e-commerce industry can break out of any geo-restrictive boundaries and attract customers from all over the world.

The best way to plan ahead and ensure as smooth a business process as possible is to examine existing use cases, along with their trials and errors. This is why it’s important to consider the following list of businesses that have leveraged blockchain technology, focusing on the benefits and the effectiveness of their transaction processes.

IBM utilizes a blockchain for supply chain management through its platform called IBM Food Trust. The platform enables all stakeholders, from producers and suppliers to retailers, to access reliable records of specific food product’s journeys through the supply chain. By providing real-time information about the origin, processing, and distribution of food items, IBM Food Trust cares for food safety, reduces the risk of contamination, and facilitates quicker response to potential issues.

The IBM Food Trust is built on the Hyperledger blockchain and has gained a certain fame across its industry for the innovative way to address fraud prevention, supply chain faults and the need for more accurate traceability. Ultimately, what this blockchain provides IBM with is fast and reliable verification of the authenticity of products, the chance to minimize waste and to build consumer trust.

Unilever and SAP, a major software company, joined forces to build a solution for Unilever’s global palm oil supply chain. They were aiming to increase the traceability and transparency in the supply chain. This process was needed as palm oil is mixed with physically identical raw materials from either verified sustainable or unverified sources, so they needed a way to keep track of the origin information of those materials.

“Unilever is committed to achieving a deforestation-free supply chain by 2023, and blockchain technology has the potential to help companies, like ours, track their supply chains to ensure the commodities we source respect people and the planet.”

– Dave Ingram, Chief Procurement Officer at Unilever

The solution that the giants came up with allows companies to tell the percentage of palm oil products they have purchased from a sustainable supplier and to track it to the final product. But that’s not where Unilever is stopping with blockchains. Unilever also completed a blockchain pilot for tracking advertising spend for the digital advertising industry. Apparently, calculating digital advertising spending is becoming a problem due to the reconciliation accounting method. By removing intermediaries, trying projects to find better ways of accounting for their spending and record sources of data, Unilever is hoping to resolve a massive issue in their advertising field.

Christie’s is a renowned British auction house that has tapped into the Web3 world numerous times. In late 2022, Christie’s announced its Christie’s 3.0 platform dedicated to on-chain NFT sales. The platform invited auctions to be hosted on the Ethereum blockchain from start to finish. Each sale within the auction is also recorded on the ETH blockchain.

“By incorporating regulatory tools, such as anti-money laundering and sales tax, we have built an inclusive solution where both veteran and new NFT collectors can feel secure in transacting with Christie’s 3.0.”

– Nicole Sales Giles, Director of Digital Art Sales at Christie’s

This is a very bold project, as it puts NFTs in the category of art forever, and it brings many Christie’s clients into the Web3 world. It allows Christie’s to tap into a new market in digital art and to invite a wider client base for auctions. This is a great way to implement blockchain into your business, to make sure that your brand’s name will always be recorded in history and to open opportunities for additional revenue streams.

With artists in mind, WMG and the NFT market OpenSea put their powers together to create more opportunities for the music industry. This partnership aims to empower musicians and creators by developing and launching innovative projects that enable artists to connect with their fans in new and immersive ways.

“Fundamental to music’s DNA, is community – its artists and fans coming together to celebrate the music that they love. Our collaboration with OpenSea helps to facilitate these communities by unlocking Web3 tools and resources to build opportunities for artists to establish deeper engagement, access, and ownership.”

– Oana Ruxandra, Chief Digital Officer & EVP at WMG

By tapping into the potential of blockchain and NFTs, WMG seeks to create unique and engaging experiences for artists within the Web3 ecosystem, unlocking new revenue streams and helping to create an ever-deeper relationship between their signed artists and their audiences. This is a great way to innovate marketing opportunities for the music industry and for the business itself, and WMG has done a great way in trying to do so.

Gucci is one of the leading fashion brands in the whole world, and with that fame, the masterminds behind the company know that entering the Web3 space would be a good business decision, which proved exactly right. Gucci has a metaverse of Web3 opportunities, from NFT collections to their own plot in The Sandbox metaverse platform, which have paved a way for the fashion industry to explore the NFT and Web3 world.

Gucci’s Web3 initiatives include limited edition NFTs, virtual fashion items, and engagement in the decentralized metaverse with an online shop bringing items from the past, present and future. This approach allows Gucci to connect with new audiences like a tech-savvy audience by offering unique digital experiences and exclusive digital assets within Web3.

With its rich history, successful improvements, and various use cases, blockchain technology represents a groundbreaking way for businesses to operate through transactions on the blockchain. By bringing so many benefits to its users, it’s hard to imagine how the blockchain can improve even more, yet it’s exciting to think about. Integration of blockchain with emerging technologies like AI and IoT will enable more sophisticated and automated transactions. As central bank digital currencies (CBDCs) gain prominence, blockchain’s role in reshaping global financial systems will get even more important. Overall, blockchain will continue to evolve, shaping the future of secure, transparent, and decentralized digital transactions.

If you want your business to be a part of that exciting future, and this article has shown you exactly why that should be, but don’t know where to start and how to move on, then DigitalArtists.com is the perfect way around that. At DigitalArtists, you can expect a team of experts which will plan every step of your journey to success and will be transparent about each step. Bringing Web3 into your business shouldn’t be a hard process for you, and an agency like DA can promise exceptional benefits like end-to-end support, safety and regulatory compliance.

An informative article on blockchain transactions, like this one, which includes details on how to track transactions and explains both confirmed and unconfirmed, is filled with important information. However, if you are someone who prefers a quick summary of the content you’ve just read, or if you’re looking for a concise version of the most important information on the topic, then these FAQs should answer all your questions.

A blockchain transaction is the transfer of digital assets or information recorded in a secure, decentralized ledger. Verified through cryptographic principles, each transaction forms a block, linked in a chronological chain. Immutable and transparent, blockchain transactions offer a tamper-resistant and traceable record, typically associated with cryptocurrencies or smart contract executions.

Transactions in blockchains can be traced due to the blockchain’s transparent and immutable nature, which allows for the tracking of transactions throughout the decentralized ledger. Each transaction is recorded in a sequential and tamper-resistant manner, providing an open and verifiable history of asset movements or data exchanges. There are also blockchain explorers, which are platforms allowing users to track various blockchain transaction data.

Bitcoin transaction confirmations take time due to the network’s block time and block size limitations. Miners compete to solve complex mathematical puzzles, and when the network is congested or blocks are full, transactions may experience delays. Additionally, the confirmation time also depends on the transaction fees that are included in the transaction. Because those represent the incentive for miners to pick transactions, higher transaction fees = bigger incentive = higher chances of your transaction to be approved faster.