We are in an age where the digital world is a big part of our daily routine. A place which includes our personal information, our hobbies and connections to people, and most importantly, our personal finances and transactions. There are new payment methods coming up constantly, with 23,000 cryptocurrencies recorded as of March 2023. And whilst those cryptocurrencies have been known to people for the last couple of years due to their increased hype, the system behind them has been in the works since 1991. The online space has been a much safer place since then.

There are monumental historical cyberattacks which have targeted millions of devices and money throughout the world. Skillful hackers have been able to breach digital systems and leave a massive negative impact on different companies. Many people are still hesitant about the idea of owning intangible currency. Especially after the boom of cryptocurrencies, it’s clear why there is a need for an unbreachable system to host them. It’s a good thing that blockchains are renowned for their security and other benefits, which have been proven to work perfectly. Let’s get into answering the important question of what a blockchain is.

A blockchain is the smart, secure and decentralized system behind cryptocurrency transactions, similar to traditional ledgers, most often used in accounting, which are books for accounting transactions. These always record dates, types of transfers, amounts of transfer and the senders and receivers of the transfers. Hence why blockchains are called digital ledgers.

The idea for a blockchain was born to generate security around digital transactions and was first used with the Bitcoin blockchain. This was done in 2009, a year after unknown creator/s called Satoshi Nakamoto created Bitcoin. This period marked the first Bitcoin transaction, when Nakamoto transferred 10 BTC to Hal Finney, who was an important person in Bitcoin’s creation. This is a historical moment, creating concrete proof that future digital transactions have a secure and reliable system to be based on, bringing attention to the world about what a blockchain is and how it can change their businesses.

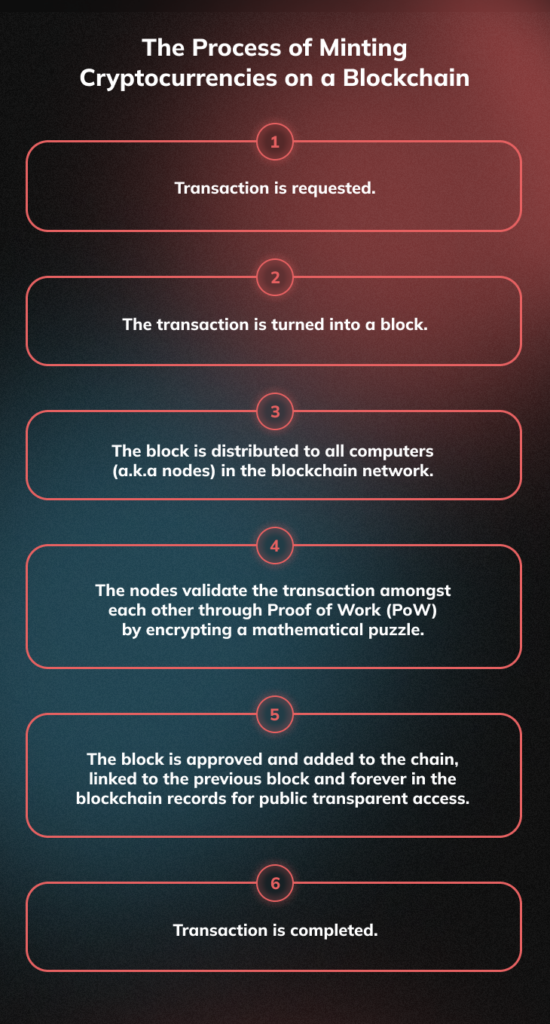

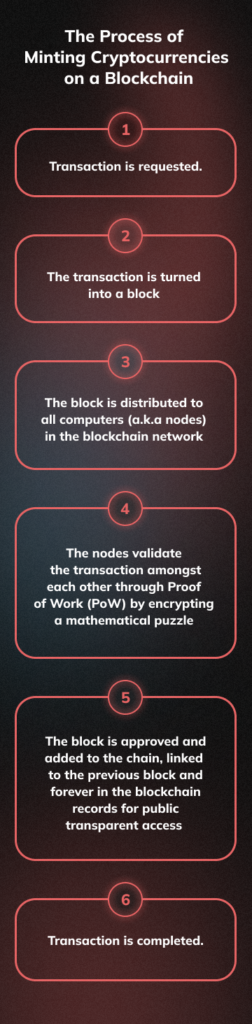

The whole process of sending or receiving Bitcoins is made straightforward by apps that don’t show how a blockchain works behind the scenes. Once the user requests the transaction to be made, the transaction is turned into a “block”. Then, a whole operation runs through a worldwide blockchain network of connected computers, also known as nodes, which receive this block. This network is called a peer-to-peer (P2P) network, which basically allows the connected users to conduct and handle the transactions within the network, without needing a middleman. These computers then need to validate the transaction between each other through the Proof of Work (PoW) method.

This verification process includes the encryption of a mathematical puzzle made of encrypted hexadecimal characters. Once this complex task is done, the transaction in the form of a block is added to the chain of blocks, connected to all other blocks and stamped in the blockchain accounts. The recipient then receives their Bitcoins.

Proof of Stake (PoS) is another mechanism used by blockchains аnd cryptocurrencies other to Bitcoin to validate transactions and is one place where blockchains and smart contracts meet. Compared to the PoW method, PoS only relies on the validators (stakers), which are randomly chosen based on how much their staked funds, and their funds are locked in special smart contracts. They then get the chance to create new blocks and approve transactions.

A single Bitcoin costs 28.302,70 USD as of October 2023. Having that in mind, most people would want an extra sense of security when pressing that transaction button. This is why blockchains exist and their security makes them so trusted in the crypto world.

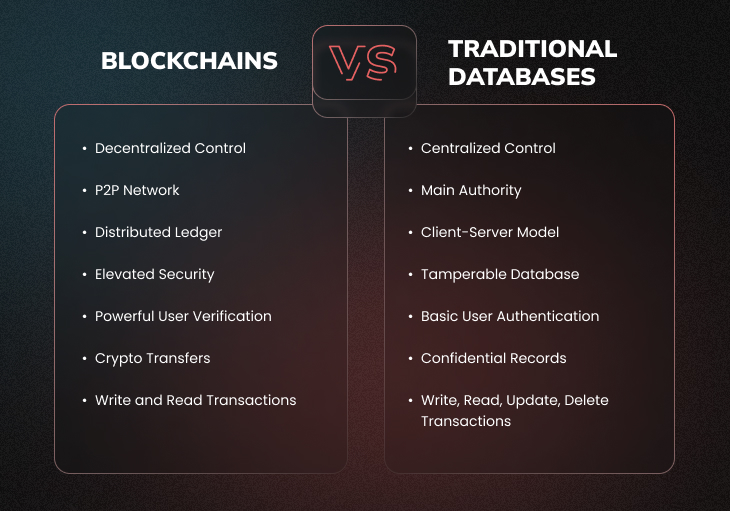

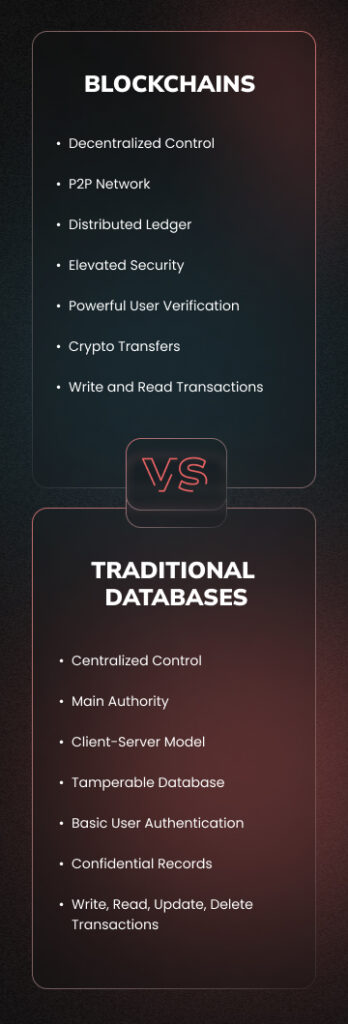

Both blockchains and traditional databases are used to store some type of information, but they come with different benefits. Online users nowadays are more likely to trust a blockchain ledger compared to traditional databases. But for some, a traditional database is better.

Blockchains are suited for cryptocurrencies and other Web3 assets like NFTs and DeFi services. Traditional databases, on the other hand, rely on centralized storage servers and their systems for confidential records or for a database structure that records more in-depth information in fixed formats of fields and rows. These have a centralized system that has central authority in control of the database.

With basic user authentication, sometimes the likes of username and password, these databases can be tampered with if they are in the hands of malicious users, unlike blockchains, which provide more elevated security with private wallets and encrypted keys. And even if the traditional database system had the same sense of security, it still might not be enough, because the records can not only be written and read like, but they can also be updated and deleted. Once a transfer is created in the blockchain then it cannot be tampered with and a record in a traditional database can be erased and deleted forever.

Traditional databases might be better for smaller businesses which would want to have complete access and control over their data. Blockchains, however, provide a more elevated security than any other database due to their security, and the benefits of that can come in masses for prosperous businesses.

Knowing what a blockchain is and why it is needed, it’s important to look at some great examples of the most secure blockchains. Having a digital ledger with top-notch security is very important, and these use cases show exactly how to create it.

Blockchains are something that many industries and businesses can profit from. By revolutionizing the way people interact digitally with finances, non-tangible products and future technology, blockchains provide a long list of benefits.

Blockchains enable the:

And just like that, you can start thinking about how your business can become even greater through blockchain technology. But first, you should consider what type of business you are running and if it is suitable to have a blockchain implementation in it.

Blockchains offer businesses robust security through their cryptographic technology and their decentralized nature. Because each transaction is sealed into the blockchain, and linked to the previous one, an unalterable chain is formed. With elevated security, blockchains are greatly resilient to attacks, and with their PoW and PoS consensus mechanisms, they make transaction validation a great tool for businesses in terms of trust, fraud reduction and the protection of sensitive data.

The decentralized nature of blockchains provides businesses with unparalleled transparency. When a transaction is made, there is no chance for it to be altered in any way, only leaving the options of writing and reading records. This is a great benefit for businesses wishing to work with collaborators, as it builds trust in all parties. Through smart contracts, as well, businesses can use smart contracts to automate agreements and thus reduce costs and disputes, whilst having all documentation transparently available to all parties.

Traditional banking systems quite often face delays in processing and completing transactions and various banking tasks. This could be due to different time zones, complex amounts of money, or any other technical difficulties. Blockchains, on the other hand, enable near-instant settlements of transactions through smart contracts. Businesses can settle worldwide deals without issues, access and move funds rapidly and tap into the global marketplace without worrying.

Geographical borders aren’t a factor for businesses when they use blockchains at all. Blockchains transcend those borders and allow for business to partner with international businesses or approach a new client base. This method ensures that business receive a diverse customer base and the expansion to foreign markets. The global trade landscape can be revolutionized through blockchains by becoming highly accessible and connected.

When the idea of blockchains was first realized, it was primarily aimed for cryptocurrencies, with Bitcoin as the prime one. Blockchain 1.0 was used as a digital ledger, but only recording the items transferred and wasn’t as reliable as the current version.

Blockchain 2.0 launched in 2014 by welcoming more than just cryptocurrencies to the technology. This opened the doors for the Ethereum (ETH) blockchain, which hosts many cryptocurrencies but also most NFTs. This version of the blockchain also introduced the ability to store and operate computer codes, which created smart contracts.

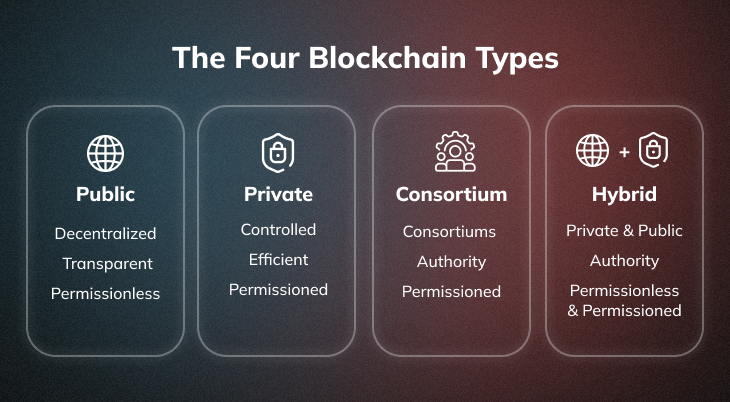

The last development so far is the Blockchain 3.0 and it is the most exciting development for all business owners. This version of the blockchain is perfect for industries looking to optimize their markets and performances. It is this version of the blockchain that will allow the most careful and secure handling of sensitive data and information for customers of any business. Even though there are different versions of the blockchain system as a whole, there are also different types of blockchains available with various features.

Public blockchains are the most used nowadays. These are completely decentralized, meaning that no authority or person controls the network. This way, anyone wishing to join the network can, be it to fact-check transactions or to contribute by making transactions which get recorded in the ledger. This provides an extra sense of security because with so many public users, more nodes are added, which are important for the validation of transactions. This means that any members of the ledger wishing to damage it will have a very hard time doing so, and they can be quickly unveiled and banned.

A private blockchain is the total opposite. There is a central authority controlling the network and deciding on what activities take place within it. Unlike public blockchains, in the private ones, network members decide who can join the network and who has control over certain processes. The validators are private, so deciphering who is who becomes harder, but the circle of members is much smaller than public blockchains. This means that transactions are approved faster and therefore consume less energy, making this type of blockchain more efficient.

A consortium blockchain includes more than one organization as the main authority controlling the network. This could be a group of companies (=consortiums) which make decisions for the network, which in a way also provides a decentralized system. As the private blockchains, nodes wishing to become members of this type of network also must be approved by the existing members. Consortium blockchains can be great for businesses as they provide a selected circle and are also more efficient, like private blockchains.

And finally, the hybrid blockchain is a mix of both public and private blockchains. This blockchain provides organizations with both private and permissioned blockchain with public and permissionless features. For example, the authority decides which data can be accessed privately and publicly – allowing for some data to be confidential whilst other can be accessible to the public.

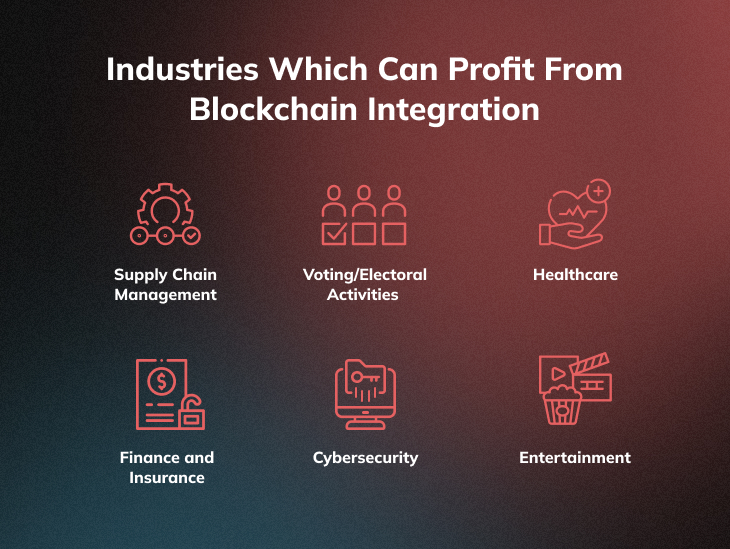

One of the most important industries which can benefit from a blockchain system is the healthcare industry. A secure and reliable blockchain technology can ensure the proper filing of digital health records of patients worldwide, which would be stored in a secured storage. This way, should any hospital or other medical party need access to those for a specific client, they can gain access and be shown all the important and potentially life-saving information. It is known of cases where health records have been misplaced, lost or even not filed out properly, which can be fatal for some clients. A secure blockchain system would resolve those issues for the industry.

Another industry to increase productivity and efficiency through blockchains is that of supply chain management. Many current industry issues can be prevented by implementing a blockchain into any SCM business. For example, tracing products through the production and distribution process can be made more reliable and easier. This would therefore prevent counterfeiting. In many ways blockchains in the SCM industry will generally improve product quality and availability for any SCM business.

The benefits of blockchains can expand even to organizations like governments. Alone in election voting this could be considered the most secure and reliable way to register and count votes. Why should people think about this option? Well, electoral fraud is a well-known problem that many countries and campaigns are facing. By implementing a blockchain in this process, tampering with the votes and the overall result is impossible.

Leading industries like finance, insurance, cybersecurity, transportation and even entertainment can all profit from having blockchain technologies implemented through the implementation of blockchain payment options. Not only that, but they can also rely on a transparent and secure ledger for their records. They can further expand into the Web3 world and grow both their catalogue of products and their clientele. Let’s look into successful examples of businesses that have made the most of blockchain systems.

Blockchains have diverse functionalities and can even be offered as Blockchain as a service (BaaS). With such a diverse portfolio of industries and benefits, blockchains have cemented their popularity in emerging business strategies all over the world. Following are five great examples of brands which have successfully implemented blockchains, one way or another, into their businesses and have profited from that.

Supply chain management often faces many issues like food fraud, poor food traceability, incorrect shelf-life prediction and overall food safety issues. This is why the big brains behind Walmart were able to track down their issues and resolve them, all thanks to the blockchain technology.

Firstly, Walmart Canada was facing a massive issue for their transportations – huge data inconsistencies in the invoice and payment processes for freight carriers. This issue created an even bigger problem for one of the biggest supply chain leaders in the country. Walmart had to constantly reevaluate payments and put even more effort than usual, but the issue of long payment delays just grew larger. The solution – a blockchain system.

The solution came in handy because as a digital ledger, the blockchain was the perfect system to introduce an automated system for managing invoices and payments to third-party freight carriers. Given that Walmart delivers over 500,000 shipment a year across Canada with both own and third-party carriers, this implementation of a blockchain was the right decision to stop a big problem and to ease the payment process throughout the transportation process.

Another great way that Walmart has tackled a major issue through the power of blockchains is that in China and their food safety issue. Back in 2016, the VP of Food Safety within Walmart requested a package of sliced mangoes to be traced. This process took 6 days, 18 hours and 26 minutes. After Walmart partnered with IBM to create a system which would ease food tracking, the process took only 2.2 seconds.

Walmart then worked with JD, IBM and the Tsinghua University National Engineering Laboratory for E-Commerce Technologies in Beijing and created the Blockchain Food Safety Alliance. This resulted in an enhanced food tracking, safety and traceability process for greater transparency across the food supply chain in China over time. Walmart has since continued to develop new blockchain technologies and to improve in efforts to create an even better and transparent food supply chain process across their networks.

Amazon is a great provider for cloud-based services, like storage, databases, AI, security and many more. Many companies have been loyal users of those services, because Amazon is established as one of the biggest brands in the entire world. Given its influence and growth strategies, it’s no wonder that Amazon is focused on a great Web3 presence, starting by offering Blockchain as a Service (BaaS).

BaaS is a service where its clients can create, run and moderate their own blockchain apps on that specific blockchain. While they’re doing that, the BaaS provider is responsible for maintaining the blockchain in order and running smoothly. It is a business opportunity based on the Software-as-a-Service (SaaS) model, which operates in a similar way but with software. Amazon saw an opportunity to create a large profit from this idea.

In 2018, Amazon announced the Amazon Managed Blockchain (AMB), with focus on easy creation and management of blockchain networks for clients. It allows companies to build Web3 applications on both public and private blockchains. These efforts proved successful quickly and it has a great list of use cases with clients like Nestlé, Accenture and Sony.

Alibaba is a worldwide known name for its digital marketplace connecting consumers and merchants. While the online marketplace launched in 1999, it gained massive recognition in recent years throughout the USA and Europe. The company has even succeeded in competing with major brands for special days like Single’s Day, Black Friday and big holiday shopping periods.

The Alibaba Group didn’t stop there, however, and released its own Alibaba Cloud services. With over 100 services like database, storage, security, analytics and AI, Alibaba Cloud was established as another global leader in cloud computing services. Like Amazon, the Alibaba Group opted to provide BaaS, by helping customers to build a secure and stable blockchain environment, save operation and maintenance costs and enable business development. Its services can be used for products provenance, meaning that clients receive support with end-to-end traceability and anti-counterfeiting during their supply chain process. This could also be enhanced through their Supply Chain Finance service, offering overall management to the supply chain by integrating transaction records, logistics and capital flow.

Alibaba’s blockchain services also offer a Data Assets Sharing service, tackling issues like data ownership determination, privacy protection and processing of large amounts of data. This service is mostly valuable for user privacy, scientific research and medical services by making their data more valuable. Finally, there’s the Digital Content Ownership service which standardizes and integrates ownership recordation and transaction. By resolving issues regarding data circulation like data traceability and data tampering, this service improves Alibaba’s clients’ methods of transactions through smart contracts.

The best example for successful blockchain integration within a finance business would be that of J.P.Morgan and its blockchain-based wholesale payments transactions platform Onyx. J.P.Morgan’s goal, through Onyx, is to transform how money, assets and information are moved around the globe. The company has several services within Onyx, all tailored to different businesses. Liink, for example, is a P2P network for information exchange.

With over 96 participants, over 95 million transactions and over 20 countries covered by the network, Liink has proven to be a successful use of blockchains for J.P.Morgan. Network participants can exchange data amongst each other whilst having complete privacy and security, maintenance of control regarding whom they connect with and what those connections have access to.

Other services the finance leader provides are Coin Systems, which are all about focusing on solutions for transferring money – mainly for multi-bank and multi-currency digital ledgers. Onyx Digital Assets is another service which acts as an exchange platform for different types of digital assets. But one main Onyx service by J.P.Morgan stands out in the whole Web3 world, and that is the Onyx Lounge.

The Onyx Lounge is part of Decentraland, one of the top metaverses currently out there, and is based within the Metajuku Mall. Metajuku alone is considered a top shopping district within the Decentraland metaverse, and is based off Tokyo’s center for street fashion, the Harajuku district. Bearing in mind its popularity withing the user base, J.P.Morgan secured a great spot to open its Onyx Lounge, but what exactly is it?

J.P.Morgan is a leading global financial services firm founded in 1799 and as of 2023, it is operating in more than 100 countries. So, what would stop this business from becoming one of the leading financial services firms in the upcoming metaverse? Absolutely nothing, and with their Onyx Lounge, this statement is being realized more and more as it is the first bank to ever enter the metaverse.

The Onyx Lounge will lay the ground for a stable metaverse presence for J.P.Morgan’s financial services with a very bright future. This is because players will rely on virtual realities more as time goes on and they will not only play in them as digital entities, but also work and make money, and naturally, spend this money. With Decentraland’s nature of buying and selling virtual plots, players will need to correspond with reliable banks to do business, and J.P.Morgan already has set the grounds for being one of the best options available.

The last use case of successful blockchain security implemented in businesses is a very important one, because it falls within the healthcare industry. In January 2022, four major companies joined forces to create an innovative system, aiming to better the healthcare industry. The Cwm Taf Morgannwg University Health Board (CTMUHB) of the National Health Service (NHS) Wales, UK, along with Roche Diagnostics, Digipharm and Life Sciences Hub Wales, used Digipharm’s blockchain platform for the purpose. They collaborated to develop a payment-by-result contracting model to pioneer sustainable procurement within the industry. The outcome of the project overall promises shorter wait times for patients, sustainable procurement policies, quicker diagnostics and a fair payment structure for the services offered.

Having such great examples of successful blockchain security implementation within businesses is great for you in order to see what power blockchains really hold. The way they can transform your business plans is truly remarkable, but it’s also important to consider the challenges that come with blockchains, and most importantly, how these can be easily tackled.

Reading about blockchains can leave you with the impression that they are this complex technology only used to store codes and cryptocurrencies. Any experienced Web3 agency can show you that actually, blockchains can be a fun and profitable implementation in your business. To elevate your business and to create a stable flow of income, blockchains can be the best new business strategy you can come across.

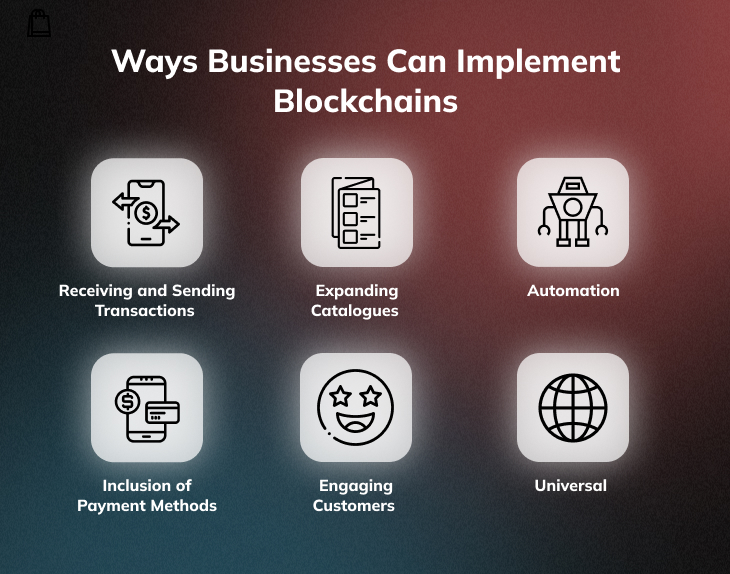

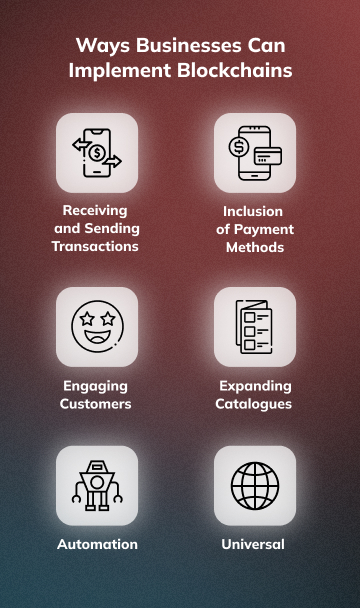

By introducing a blockchain system to your business, you are ensured to grow in many ways. You will ease the process of receiving and sending transactions and through including both crypto and fiat currencies, you will ensure that more people can pay for your business. Blockchains are also the gateway to Web3 and everything it offers, so the option to expand your current catalogue of products just got easier. You can thus tap into various industries, collaborate with them and invite their clients to your business.

Many businesses can also profit from being automated, or at least to have certain systems automated, which will boost their productivity. And this combined with the blockchain technology being universal, they can open a door for worldwide investors. All these things are concentrated on your most important asset – your customers! Everything that blockchains bring to your business is set to improve how you interact with your customers and in return, how they invest in your business.

Not all cryptocurrencies are blockchain-based, some like the IOTA and Nano currencies are based on Directed Acyclic Graphs (DAGs). DAGs promise to eliminate mining fees, which on normal blockchains can sometimes be very high, and to also speed up transactions. As good as that might sound, one thing sets blockchains apart from DAGs, and that’s the security.

DAGs are more vulnerable to certain types of attacks, and that is why the biggest and most expensive crypto currencies like the BTC and ETH are kept hosted on blockchains. Cryptocurrencies have seen highs and lows, but the businesses around them have learned how to create more revenue streams through crypto in blockchains.

Been a member since mint day but meeting @rodolitz @chefcapon & @ConorHanlon83 in person made me realise that @Flyfishclub is way bigger than what I initially thought it was!

— Robin Raj (@robin_raj5) May 20, 2023

A really great bunch of humble founders. Can’t wait for grand opening in Dec 2023! #VeeCon2023 pic.twitter.com/FtuFmPElWA

Another way businesses can tap into the blockchain world is through the Internet of Things (IoT). The IoT represents computing devices which are connected to each other like computers, smart watches, phones, TVs and even modern refrigerators. The important part of the IoT is that these devices collect and exchange data with one another. Now, bearing that in mind, that information can be very confidential, or even if it isn’t, there must be a way to ease the general sense of security for a product’s customers. That is where the connection between the IoT and blockchains comes into play. Once the IoT is enabled to share data through a blockchain, all those records are ensured to be encrypted and safe within the blockchain.

The choice of the right blockchain type is important for any business wishing to provide (application) services through an IoT-blockchain system. Private blockchains, collaborated with IoT, can allow businesses to decide on the network participants and what type of information they can access. And in the scenario of a consortium blockchain, many businesses can collaborate to exchange databases reliably and to improve their services together. Let’s take a deeper look into how big brands have successfully taken advantage of the security aspects of blockchains and how they have created new businesses around those.

Blockchains, through regular security updates, additional security, smart contracts and in general the way they operate, are the one of the most secure digital systems. Blockchain companies are constantly on the lookout for issues within blockchains and are helping to keep systems as secure as possible. This constant cycle of improvement ensures that blockchain technology is one of the most trusted in the digital world and ensures a great future for blockchains.

Businesses from a large list of industries have the potential to benefit from blockchains. Understanding blockchains could be complicated for you, but understanding their potential and how your business can gain from them should already be clear. In such cases, it is best to collaborate with an experienced agency like Digital Artists with a team of professionals who understand the Web3 world and have the portfolio to prove it.

This ultimate guide answers what a blockchain is, what the benefits of using it are and how to successfully implement it in your business. Here are some of the main topics summarized for the ones who want a quick read over the topic.

A blockchain is a digital and decentralized ledger which records the transactions of cryptocurrencies. The idea for a blockchain was born to generate security around digital transactions and was first used with the Bitcoin blockchain. Being decentralized means that not one person/organization controls the blockchain, but all members have access to the information available in the blockchain, like the transactions, their amount and type, when they happened and their senders and receivers.

The process behind the blockchain technology begins with the transactions, referred to as blocks. A worldwide blockchain network of nodes, the connected computers, receive this block and as part of their work, they are conducting and handling the transactions without a middleman. This peer-to-peer network (P2P) validates the transaction between each other through a Proof of Work (PoW) or Proof of Stake (PoS) validating mechanism. The first one requires the encryption of a mathematical puzzle, after which the block is verified and added to the chain of block. The latter mechanism relies on the validators to have staked funds, and chosen at random, one of them will create the block and approve the transaction. Once this is done, the block is forever in the blockchain and the recipient will receive the money.

BaaS is a great way to save on costs Pas it provides a solution removing the need for in-house infrastructure. It also has pre-built solutions tailored to your business and can easily quicken blockchain adoption into your business model. BaaS also saves you energy on looking for technical expertise as it comes with all the tools you need, and it makes blockchains an even more accessible application for your needs.